Chapter 1 Exercises

\(\require{enclose}\)

1.1 Chapter 2 Exercises

Exercise 2.3.1. Gompertz-Makeham and Survival Probabilities. Recall the U.S. Life Expectancies introduced in Section 2.1:

| Age | Total | Male | Female | Hispanic..Total | Hispanic..Male | Hispanic..Female |

|---|---|---|---|---|---|---|

| 0 | 78.6 | 76.1 | 81.1 | 81.8 | 79.1 | 84.3 |

| 20 | 59.4 | 57.0 | 61.8 | 62.5 | 59.9 | 64.9 |

| 40 | 40.7 | 38.7 | 42.6 | 43.5 | 41.2 | 45.5 |

| 60 | 23.3 | 21.7 | 24.7 | 25.5 | 23.6 | 27.0 |

| 80 | 9.2 | 8.4 | 9.8 | 10.5 | 9.4 | 11.1 |

Section 2.3 used these data to fit a Gompertz-Makeham distribution for female lives; in this exercise, we repeat this analysis but for male lives. To this end,

- Fit a Gompertz-Makeham model to the provided US Male life expectancies.

- Plot the resulting force of mortality and the survival function, compare to the one for U.S. Females from Section 2.3.

- Determine the resulting model to determine the probabilities that a 20 year old survives to age 60, 70, and 80: \(~_{40}p_{20}\), \(~_{50}p_{20}\), and \(~_{60}p_{20}\).

Exercise 2.3.1 Solution

Exercise 2.4.1. Creating a Life Table from One-Year Central Decrements. In this exercise, we will create a life table based on one-year central decrements using data from the Human Mortality Database.

- Download the data from Appendix Section 3.1. Create a subset of the data for year 2015 using female rates.

- From these central death rates, create one-year mortality rates.

- Starting with 100,000 lives at age 0, create a life table. Use \(\omega=111\) as the limiting age. List the first six rows of your table.

Exercise 2.4.1 Solution

1.2 Chapter 3 Exercises

Exercise 3.2.1. Whole Life Actuarial Present Values.

In Exercise 2.4.1, we learned how to create a life table based on one-year central decrements using data from the Human Mortality Database. In this exercise, we use this life table to explore life insurance calculations in R. We first include columns for \(A_x\) – the actuarial present values for whole life insurance – and the corresponding second moment. We then use this information to determine term and endowment insurances. Finally, we calculate the expected value and variance for an increasing whole life insurance.

Adding Columns for \(A_x\) and \(^2A_x\)

We continue by adding columns for \(A_x\) and \(^2A_x\). For that, we need to fix the interest rate. Given currently low rates, we choose \(i=2\%\).

We then determine \(A_x\) and \(^2A_x\) via their recursion relationships, where we start with \(\omega = 111\) for which \(A_{\omega}=v\) and \(^2A_{\omega}=v^2\):

R Code to Determine Whole Life Actuarial Present Values

Here is an excerpt of our now more complete life table:

Year_start Age mx qx l Ax TwoAx

1817 2015 40 0.001388 0.001387037 975424.0 0.4382283 0.2072597

1818 2015 41 0.001470 0.001468920 974071.1 0.4462248 0.2145435

1819 2015 42 0.001621 0.001619687 972640.2 0.4543477 0.2220684

1820 2015 43 0.001736 0.001734494 971064.9 0.4625642 0.2297924

1821 2015 44 0.001861 0.001859269 969380.6 0.4708978 0.2377539

1822 2015 45 0.002044 0.002041912 967578.2 0.4793477 0.2459572Term and Endowment Insurance

Let’s use it for pricing life insurance contracts. Let’s set \(x=40\) and \(n=20\), and evaluate pure endowment, term life, and endowment insurance:

R Code to Determine Whole Life Actuarial Present Values

Let’s also calculate corresponding standard deviations (square roots of variances):

R Code to Determine Standard Deviations

Increasing Insurance

Let’s determine the present value of an increasing insurance policy, using the basic summation, \[ (IA)_x = \sum_{k=0}^{\omega} {_kp_x}\,q_{x+k}\,v^{k+1}\,(k+1). \] Here it is:

IA40 <- 0

for (j in 1:70){

IA40 <- IA40 + j * dat_2015_fem$l[40+j]/dat_2015_fem$l[41] * dat_2015_fem$qx[40+j] * v^j

}

IA40 <- IA40 + dat_2015_fem$l[111]/dat_2015_fem$l[41] * (71 * dat_2015_fem$qx[111] * v^(71) + 72 * (1-dat_2015_fem$qx[111]) * v^(72))

IA40[1] 17.46758Alternatively, we can evaluate the increasing insurance present value as the sum of deferred insurance contracts:

\[ (IA)_x = \sum_{k=0}^{\omega} {_{k|}A_x}. \]

Carrying it out…

BarjA40 <- rep(0,72)

IA40_2 <- 0

for (j in 1:71){

BarjA40[j] <- dat_2015_fem$l[40+j]/dat_2015_fem$l[41] * v^(j-1) * dat_2015_fem$Ax[40+j]

IA40_2 <- IA40_2 + BarjA40[j]

}

BarjA40[72] <- dat_2015_fem$l[111]/dat_2015_fem$l[41] * (1 - dat_2015_fem$qx[111]) * v^(72)

IA40_2 <- IA40_2 + BarjA40[72]…we get the same result:

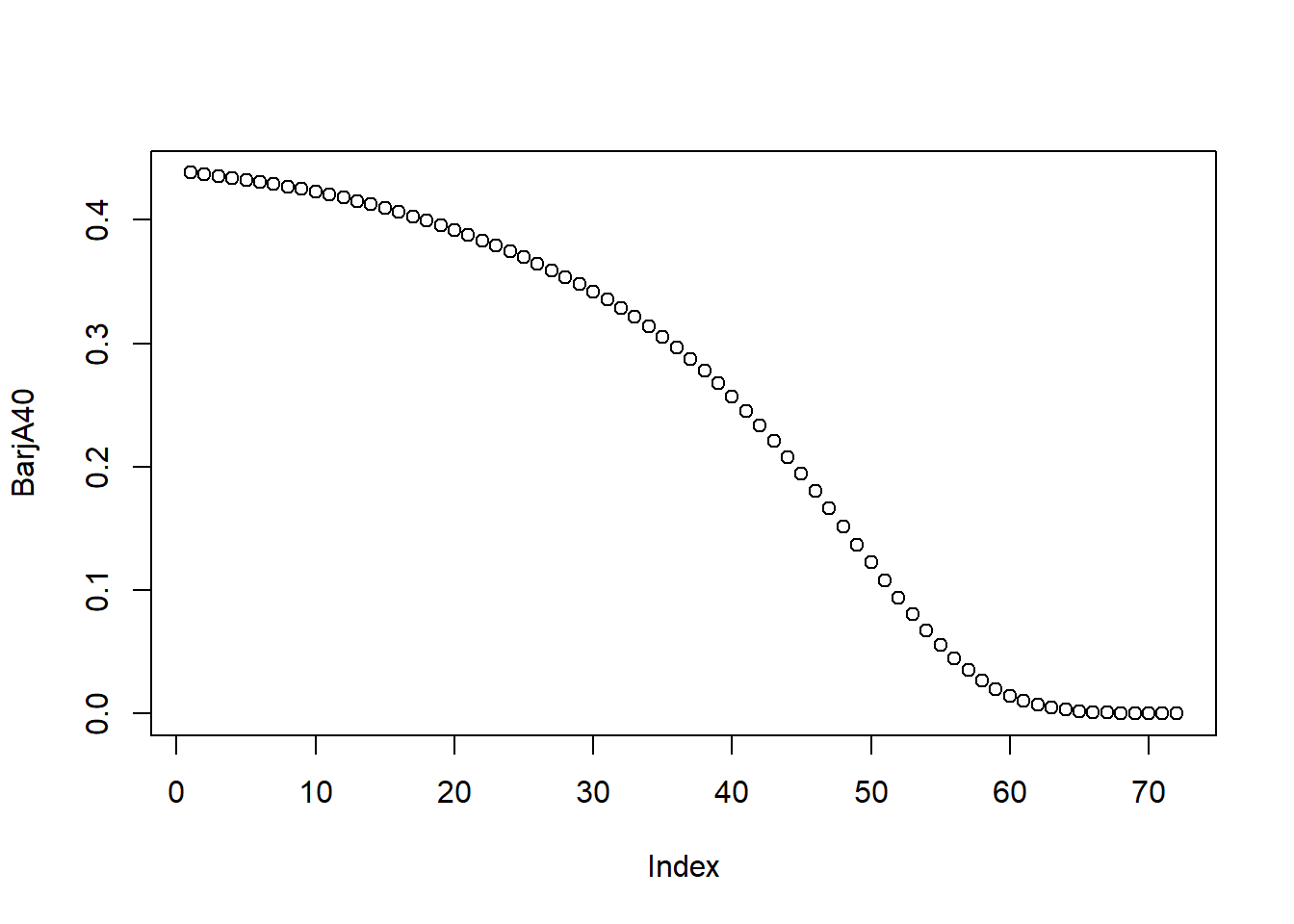

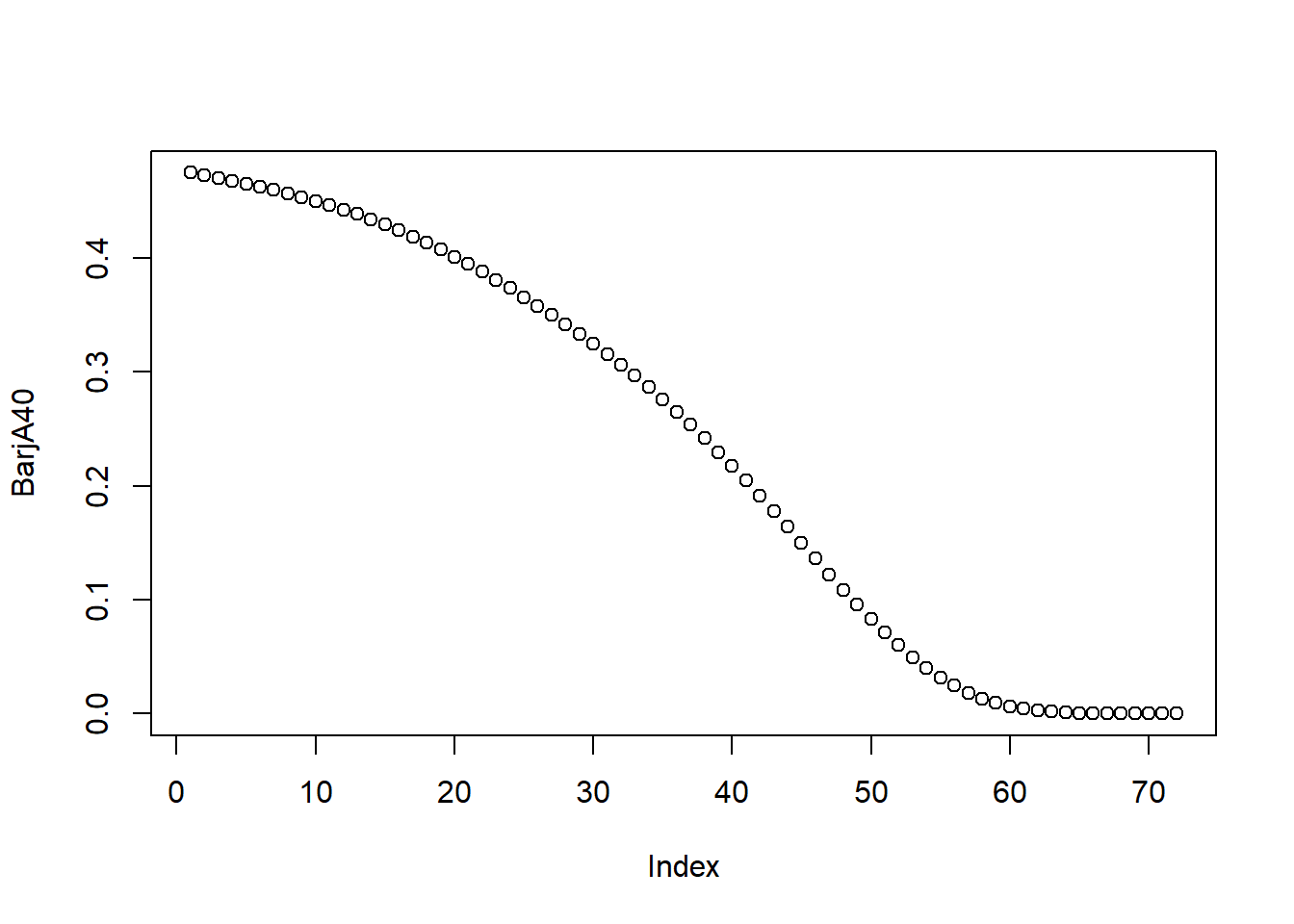

[1] 17.46758We can also plot the deferred insurance actuarial present values:

Let’s also evaluate the second moment, which we obtain by squaring the payoff and the discount factors:

SecondMomIA <- 0

for (j in 1:70){

SecondMomIA <- SecondMomIA + j * j * dat_2015_fem$l[40+j]/dat_2015_fem$l[41] * dat_2015_fem$qx[40+j] * v^(j*2)

}

SecondMomIA <- SecondMomIA + dat_2015_fem$l[111]/dat_2015_fem$l[41] * (71 * 71 * dat_2015_fem$qx[111] * v^(71*2) + 72 * 72 * (1-dat_2015_fem$qx[111]) * v^(72*2)) We can use it to determine the standard deviation:

[1] 2.4100411.2.1 On your Own

Repeat the above calculations above for the US male population. To this end, you should:

- complete the male life table with columns for \(A_x\) and \(^2A_x\);

- determine pure endowment, term life, and endowment insurance values and standard deviations for a forty year old male and a 20 year term; and

- determine the value and the standard deviation for an increasing whole life insurance on a 40-year old male insured.

R Code to Determine Whole Life Actuarial Present Values

1.3 Chapter 4 Exercises

Section 4.3 Exercises

Exercise 4.3.1. Actuarial Present Values for Select and Ultimate Tables. The select and ultimate tables introduced in Section ?? are complicated – is such complexity is warranted in practice? To get insights into this question, in this exercise you will compare actuarial present values derived from select and ultimate mortality to those from only ultimate mortality. To be specific, we focus consider whole life insurance for using the female Canadian experience introduced in Section ??; the data are available in Appendix Section 3.4.

For these data,

- produce \(A_x\) for \(x=50, \ldots, 65\) using an interest rate of \(i=0.04\) based on

- select and ultimate mortality

- ultimate mortality

- compare these two sequences of actuarial present values by calculating their ratio.

- repeat parts (a) and (b) using an interest rate \(i=0.02\).

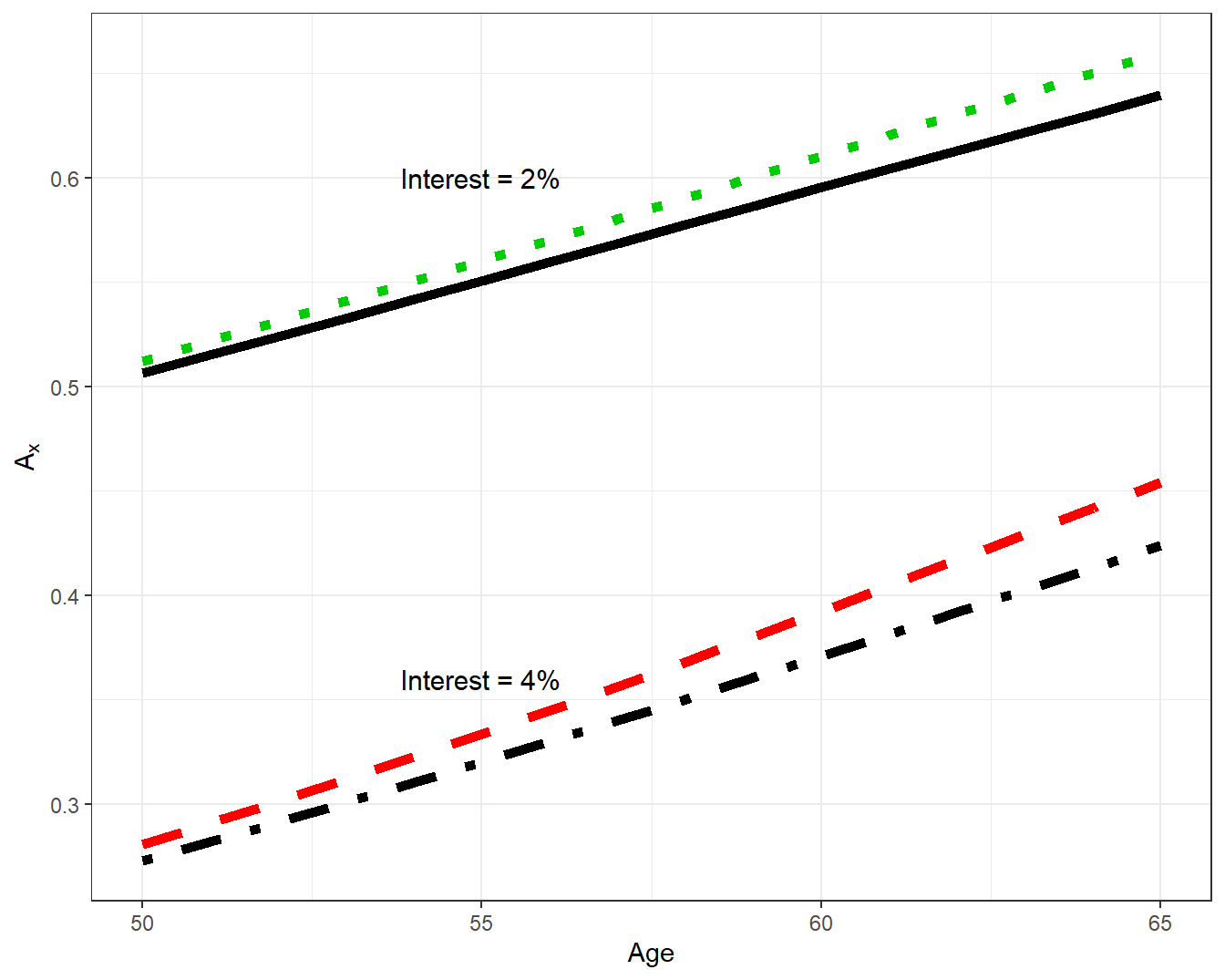

To give you a feel for the results, Figure 1.1 summarizes the results.

Figure 1.1: Life Insurance APV by Age, Interest, and Mortality Type. A plot of life insurance actuarial present value \(A_x\) by age \(x\). The top two lines are based on \(i=0.02\), the bottom two based on \(i=0.04\). For each pair, the top line uses ultimate mortality, the bottom line is based on select and ultimate mortality

Exercise 4.3.1 Answer

Section 4.5 Exercises

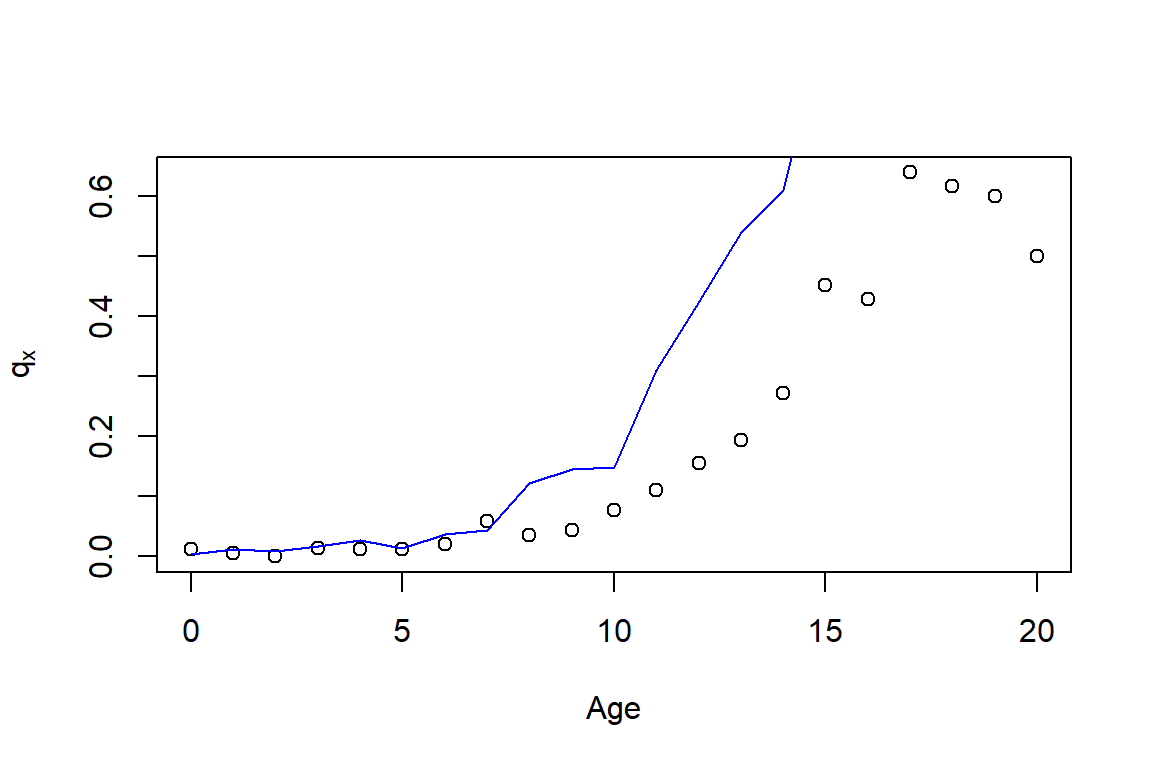

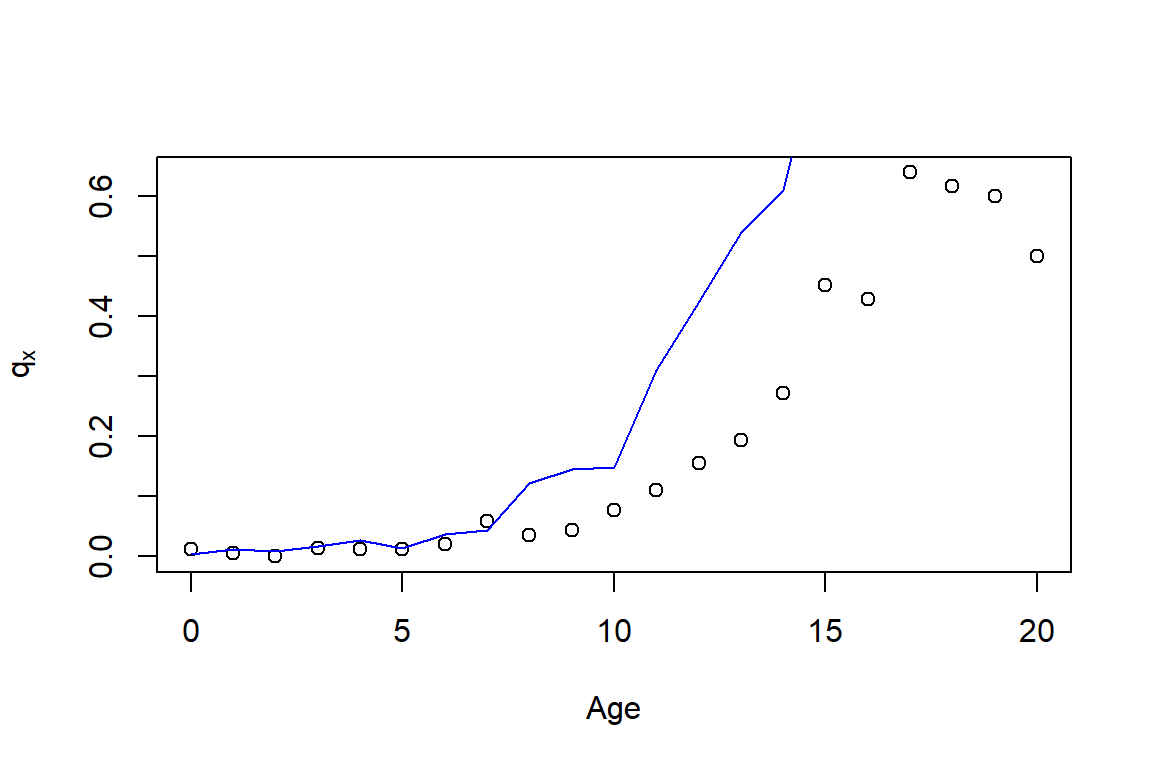

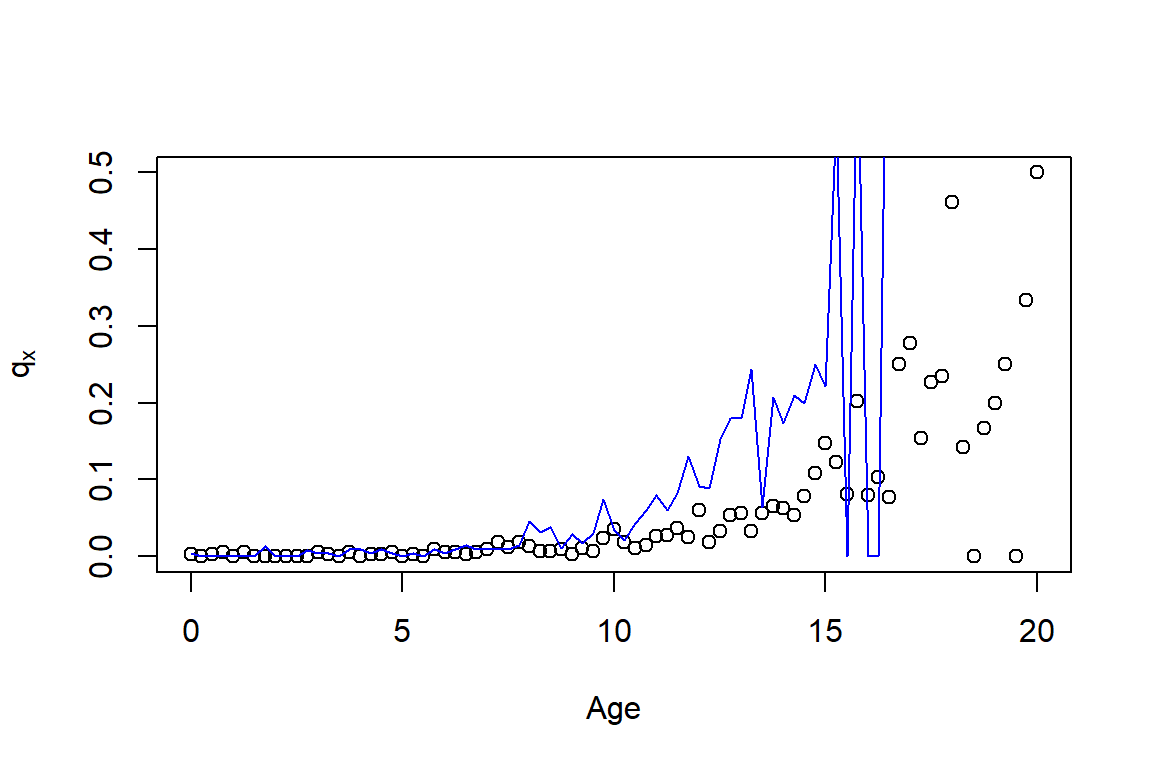

Exercise 4.5.1. Dog Survival Distributions and Actuarial Present Values. The analysis in Section ?? suggests that breed is an important factor for dog survival. To underscore this point for a broader audience, let us look at survival for a type of small dog, a “Jack Russell Terrier”, and a large dog, a “German Shepherd Dog”. We can make differences in survival distributions between small and large dogs even more meaningful by also computing selected actuarial present values that summarize future expected costs.

You should begin your analysis by downloading the data, available in Appendix Section 3.3.

The data have been re-worked so that they can be used for your analysis. Here is a bit more code needed to convert data fields appropriately and to separate the file into two subsets, one for Terriers and one for German Shepherds.

Show R Code to Pre-Process the Data

For these data:

- Compute one-year mortality rates for both Terriers and German Shepherds. Do this over \(x=0, \ldots, 20\). Graph the results.

- Because you may be working with products with events occurring more frequently than once a year, you decide to follow the strategy introduced in Section ?? and look at mortality rates occurring on a quarterly basis. Repeat the analysis from part (a) using quarterly rates.

- The results of earlier analyses indicate substantial volatility in the both quarterly rates and annual rates at later ages. One approach to mitigate this volatility is to smooth the rates. A simpler approach is to use longer periods (hence increasing exposure and reducing volatility). Repeat the analysis in part (a) using rates on a once every two year basis.

- To see how these rates might be used, you decide to repeat the analysis in Section ?? and compute an actuarial present value of the lifetime cost of surgical vet care. Use the same assumptions as in that section with the initial annual cost as 458, \(i=0.03\) interest rate and a 11 percent annual growth in surgical care costs. However, use the dog mortality from part (a). Do this for \(x=2, 5, 12\), for both breeds. You will see that that your results on German Shepherds differ slightly from those presented in Section ??; comment on why this is so.